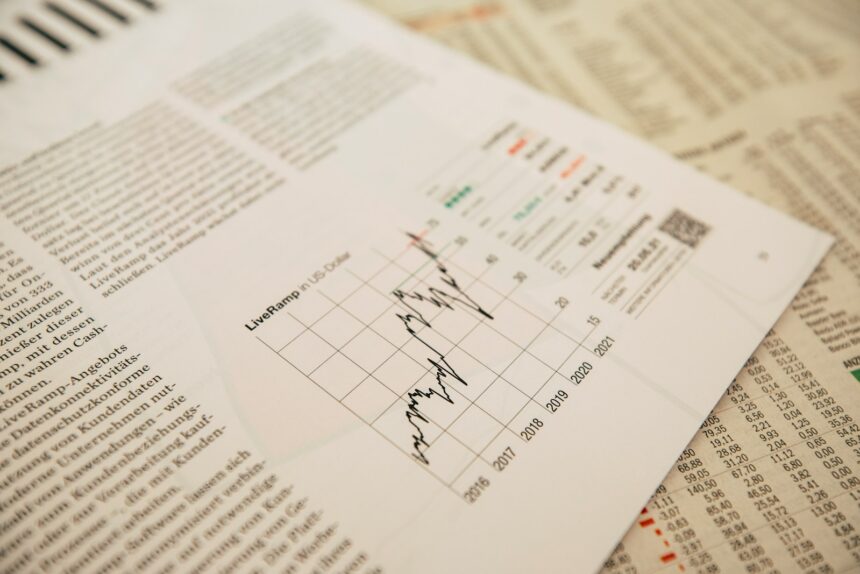

Market impact – price effect of trading

Executing a large order directly influences asset valuation by shifting supply-demand balance and consuming available liquidity. The immediate consequence is an increase in transaction cost beyond visible fees, driven primarily…

Soil carbon – agricultural sequestration tracking

Enhancing carbon storage in farmland is achievable by adopting regenerative practices that increase organic matter and microbial activity. Research shows…

Protocol design – communication framework development

Message format standardization is the cornerstone of any effective interaction scheme. Defining clear syntax and semantics ensures that data transmitted…

Database theory – data management principles

Applying relational algebra provides a precise framework for querying and transforming structured information, enabling rigorous manipulation without ambiguity. The relational…

Blind signatures – privacy-preserving authentication

Utilize Chaum’s protocol to issue anonymous credentials that maintain user confidentiality while ensuring the validity of digital attestations. This approach…